Tax Tip Tuesday: Deduct Mortgage Interest and Maximize Your Homeownership Tax Benefits

For many taxpayers, homeownership comes with one major financial benefit beyond building equity: potential tax deductions. One of the most commonly used itemized deductions is the mortgage interest deduction, which may allow eligible homeowners to reduce taxable income by deducting interest paid on qualified home loans.

In this week’s Tax Tip Tuesday, we’re breaking down how to deduct mortgage interest, who qualifies, and why understanding itemized deductions can play an important role in your overall tax strategy.

What Is the Mortgage Interest Deduction?

The mortgage interest deduction allows eligible taxpayers to deduct interest paid on qualified mortgage debt tied to a primary or secondary residence.

Currently, interest on up to $750,000 of qualified mortgage debt may be deductible for many taxpayers who itemize deductions.

This deduction can apply to:

- Primary homes

- Certain second homes

- Mortgages used to buy, build, or substantially improve a home

For official IRS guidance, review the IRS information on Home Mortgage Interest Deduction and Publication 936

Who Qualifies to Deduct Mortgage Interest?

To claim the mortgage interest deduction, several conditions generally must apply:

- You must be legally responsible for the debt

- The mortgage must be secured by a qualified home

- You must itemize deductions on Schedule A

- The loan proceeds must have been used appropriately

Taxpayers who claim the standard deduction instead of itemizing may not benefit from this deduction.

Because standard deduction amounts have increased in recent years, evaluating whether itemizing still makes sense is important.

Understanding the $750,000 Mortgage Debt Limit

For many current mortgages, the IRS limits deductible interest to interest paid on up to $750,000 of acquisition indebtedness for married couples filing jointly.

This generally applies to loans used to:

- Buy a home

- Build a home

- Substantially improve a home

Different rules may apply to:

- Older mortgages originated before certain tax law changes

- Married taxpayers filing separately

- Home equity loans used for non-home-related purposes

Taxpayers with more complex situations should carefully review IRS guidance or consult a qualified tax professional.

When Does Itemizing Make Sense?

The mortgage interest deduction is only beneficial if your total itemized deductions exceed the standard deduction.

Itemized deductions may include:

- Mortgage interest

- State and local taxes (subject to SALT limitations)

- Charitable contributions

- Certain unreimbursed medical expenses

Taxpayers evaluating whether to itemize may also benefit from reviewing our related posts on:

- Deducting unreimbursed medical expenses

- Head of Household filing status

- Health Savings Account (HSA) tax strategies

Common Mortgage Interest Deduction Mistakes

We frequently see taxpayers encounter problems because they:

- Assume all mortgage-related interest is deductible

- Forget to itemize deductions

- Misunderstand home equity loan rules

- Fail to maintain proper records

- Overlook refinancing implications

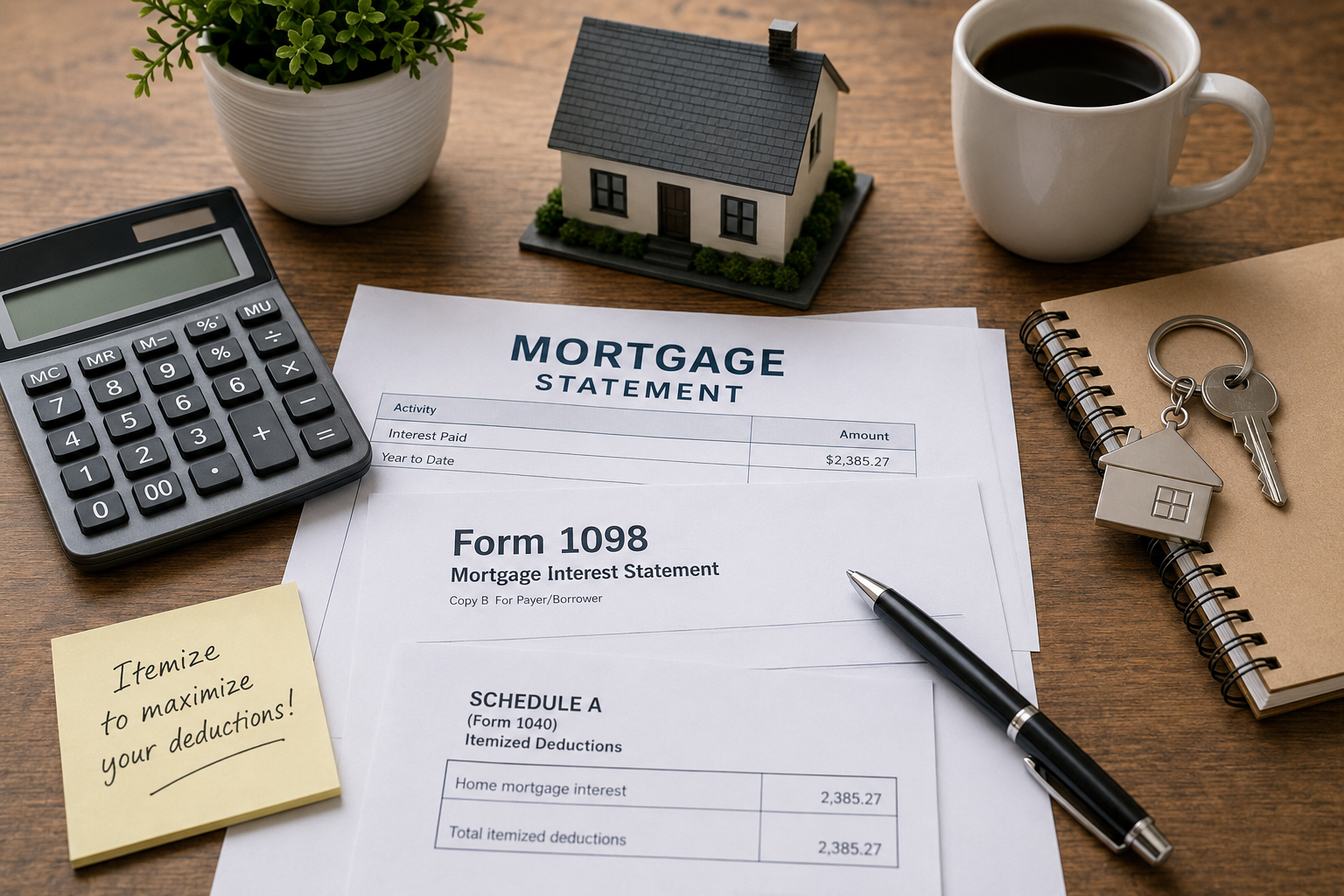

It’s important to review annual Form 1098 Mortgage Interest Statements carefully and ensure loan usage aligns with IRS requirements.

Special Considerations for Home Equity Loans

Home equity loan interest may still qualify—but only if the funds are used to buy, build, or substantially improve the home securing the loan.

Using home equity funds for:

- Credit card debt

- Personal expenses

- Vacations or unrelated purchases

may make the interest non-deductible.

This distinction is often misunderstood and can create filing errors.

How the Mortgage Interest Deduction Fits Into Your Tax Strategy

The mortgage interest deduction should be reviewed as part of a broader tax planning strategy.

It often interacts with:

- Filing status decisions

- State and local tax deductions

- Medical expense deductions

- Charitable contribution planning

- Estimated tax planning

Strategically evaluating your deductions annually can help maximize tax efficiency while avoiding missed opportunities.

Key Takeaways: Mortgage Interest Deduction

- Mortgage interest may be deductible if you itemize deductions

- Interest on up to $750,000 of qualified mortgage debt may qualify

- The mortgage must be secured by a qualified home

- Home equity loan rules are more restrictive than many taxpayers realize

- Proper documentation and annual review are essential

Need Help Determining Whether to Itemize?

Tax deductions tied to homeownership can become complex—especially when refinancing, multiple properties, or changing income levels are involved.

Cheshier Tax Resolution works with individuals and families to evaluate deductions, maintain compliance, and identify opportunities to improve overall tax outcomes.

FAQs

What is the mortgage interest deduction?

The mortgage interest deduction allows eligible taxpayers to deduct interest paid on qualified mortgage debt tied to a primary or secondary home.

How much mortgage debt qualifies for deduction?

For many taxpayers, interest on up to $750,000 of qualified mortgage debt may be deductible.

Do I have to itemize deductions to deduct mortgage interest?

Yes, you must itemize deductions on Schedule A to claim the mortgage interest deduction.

Can I deduct home equity loan interest?

Possibly. Home equity loan interest may qualify if the funds were used to buy, build, or substantially improve the home securing the loan.

What form reports mortgage interest paid?

Mortgage lenders generally issue Form 1098 showing the amount of mortgage interest paid during the year.

Is mortgage interest deductible on a second home?

In some cases, yes. Interest on qualified second homes may still be deductible if IRS requirements are met.

Stay Connected

Stay connected with Cheshier Tax Resolution for updates on community involvement, tax law changes, and insights that help taxpayers stay compliant and informed – we invite you to subscribe to our monthly newsletter.

Our newsletter delivers:

- Updates on tax law changes

- Insights from real resolution cases

- Proactive planning strategies

- Important filing deadlines and compliance reminders

- Company announcements and celebrations